ISUPETASYS (007660)

A Genuine Source of Confidence

This Year is for Corporate Transformation, Next Year is for Revenue Growth

We forecast consolidated revenue of KRW 308.0 billion (+4% QoQ) and operating profit of KRW 61.0 billion (+4% QoQ, OPM 20%) for 4Q25, driven by the sustained strong demand relative to CAPA. The company reported earnings that exceeded consensus in the third quarter. This was largely due to the full-scale reflection of revenue from G Company’s 7th generation TPU. The partial commencement of operations at the Fifth Plant (Fab 5) also brought forward the effect of the Phase 1 capacity expansion by one quarter compared to prior expectations. We understand that sales across the board, including AI accelerators and network switches, increased evenly. The Chinese subsidiary also saw its 3Q revenue increase by 17% QoQ as it shifted to new server models, and its profit margin recovered to the 18% level. We expect revenue from AI accelerators and network switches to drive the company’s overall sales in the fourth quarter.

Faster Growth Expected Next Year

We forecast consolidated revenue of KRW 1.44 trillion (+32% YoY) and operating profit of KRW 285.9 billion (+37% YoY, OPM 20%) for 2026. The full effect of the Fab 5 capacity expansion will be fully reflected starting from 1Q 2026. Additionally, we expect a further increase in ASP (Average Selling Price) due to increased performance requirements following the adoption of Rubin. This is projected to lead to sequential quarterly earnings growth. Petasys (separate entity) revenue is expected to grow by 35% YoY.

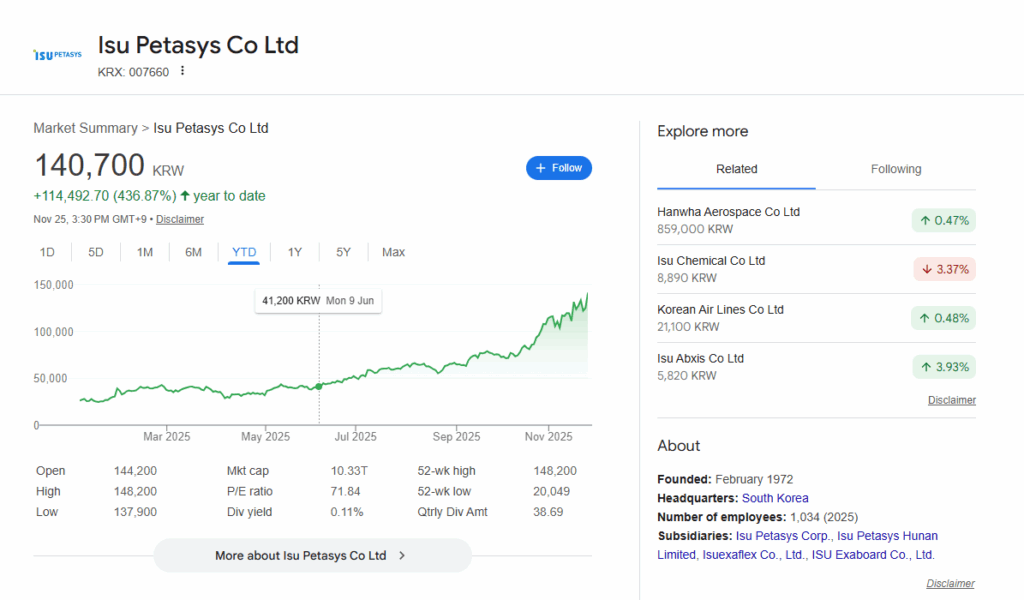

Investment Opinion: Buy, Target Price Raised to KRW 154,000

In the medium to long term, the company has presented a revenue guidance of KRW 1.5 trillion for 2029, when the Fab 5 ramp-up is fully reflected. Considering the strong demand relative to CAPA and the CAPA loss resulting from the transition to multi-layer PCB (Multi-Layer Board), we believe that the possibility of additional CAPA expansion before 2029 cannot be ruled out. The proportion of multi-layer samples, based on Petasys’ separate entity figures, also increased from 21% in 2024 to 39% in 3Q25. Having already established itself as a key value chain partner for major ASIC companies, including G Company, we raise the Target P/E to 42x to reflect the corporate transformation that will accelerate earnings growth next year. By applying the Target P/E to the 2026F estimated EPS of KRW 3,646, we raise the target price to KRW 154,000.

Link for other website: