Korean Robotics stocks Introduction: Emerging Opportunities in Korean Industrial Stocks

While global investors focus heavily on Korean semiconductors and biotech, two industrial powerhouses are quietly positioning themselves for significant growth: SPG in robotics components and Hanwha Engine in marine propulsion systems. This comprehensive analysis explores why these K-stocks deserve attention from international investors seeking exposure to Korea’s advanced manufacturing sector.

SPG: Korea’s Leading Robot Reducer Manufacturer

Company Overview and Market Position

SPG has emerged as a critical player in the global robotics supply chain following its collaboration announcement with LG Science Park in robot actuator development. Unlike typical theme stocks that surge on speculation, SPG possesses substantial technological capabilities that position it as a genuine industry leader.

https://youtu.be/l-ttFp0ZlfQ?si=CTuvyyRbGZIC52hL

Core Competitive Advantage: Full Reducer Lineup

SPG stands as Korea’s only company capable of mass-producing both SR and SH reducers, the essential joint components that enable precise robot movement. Reducers are critical devices that decrease motor rotation speed while amplifying torque, allowing robots to perform delicate and powerful movements with accuracy.

Market Context: Japanese companies Harmonic Drive Systems and Nabtesco have historically monopolized 90% of the global reducer market. SPG’s domestic production capability represents a strategic breakthrough for Korean robotics independence.

Product Portfolio Analysis

| Reducer Type | Application | Key Features | Market Opportunity |

|---|---|---|---|

| SR Reducer | Large industrial robots | Heavy-load capacity for traditional manufacturing robots | Established market with steady demand |

| SH Reducer | Humanoid & collaborative robots | Ultra-precise control for delicate joint movements | High-growth segment aligned with industry trends |

| Planetary Reducer | QDD Actuators | Lightweight, flexible design for next-gen robots | Emerging technology with exponential potential |

Industry Trends Favoring SPG

The robotics industry is undergoing a fundamental shift from heavy, powerful industrial robots toward lightweight, flexible collaborative robots and humanoids. This evolution creates a perfect market environment for SPG’s diversified product lineup.

Key Trend: QDD (Quasi-Direct Drive) Actuators

QDD actuator systems are gaining prominence in next-generation robotics due to their:

- Enhanced flexibility and safety for human-robot collaboration

- Reduced weight for mobile and humanoid applications

- Improved energy efficiency

SPG’s ability to produce planetary reducers specifically designed for QDD systems positions the company at the forefront of this technological transition.

Strategic Value Chain Expansion

SPG has announced plans to move beyond component supply and manufacture complete QDD actuators. This vertical integration strategy is significant because:

- Actuators represent 60-70% of total robot manufacturing costs

- Moving up the value chain substantially increases profit margins

- Direct actuator production strengthens customer relationships and market position

This expansion represents a long-term growth catalyst that could multiply SPG’s revenue potential in the emerging humanoid robot market.

Investment Strategy for SPG

Technical Analysis:

- Buy Zone: Below ₩54,000

- Price Target: ₩65,000 (20% upside potential)

- Stop Loss: ₩43,000 (risk management level)

Investment Thesis:

- Unique technological capability in domestic market

- Positioned for humanoid robot industry growth

- Value chain expansion strategy

- Strong partnership with LG Science Park

Hanwha Engine: The Overlooked Shipbuilding Beneficiary

Market Context: Why Engine Manufacturers Outperform

While Korea’s Big 4 shipbuilders have experienced stock price consolidation, marine engine manufacturers are receiving heightened investor attention. Hanwha Engine exemplifies this trend, combining high-profit structure with emerging growth drivers.

https://youtu.be/qm9tEbrSgbI?si=UKobpslI0VJzjh3R

Earnings Visibility and Margin Expansion

Hanwha Engine’s primary investment appeal lies in its strong earnings visibility. In shipbuilding operations, engines are installed mid-construction, meaning orders secured at elevated prices during the industry upcycle are now flowing through to actual revenues.

Key Profitability Drivers:

- DF (Dual Fuel) Engine Mix Improvement

- Dual-fuel engine adoption is accelerating industry-wide

- DF engines now comprise over 90% of order backlog

- Higher complexity commands premium pricing

- ASP (Average Selling Price) Enhancement

- Eco-friendly vessel demand drives high-value product sales

- Environmental regulations mandate advanced engine technology

- Price premiums for emissions-compliant systems

- Ship Price Correlation Effect

- Engine pricing is linked to overall vessel prices

- Shipbuilding upcycle benefits transfer directly to engine margins

- Multi-year order books lock in favorable pricing

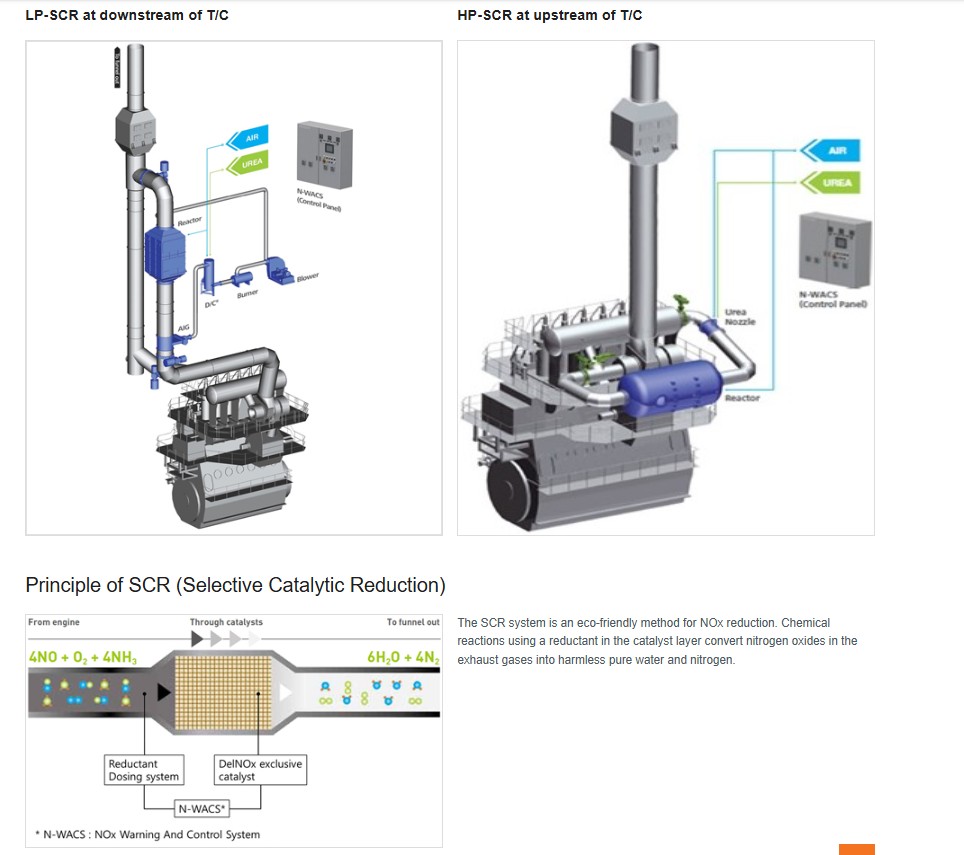

New Growth Engine: 4-Stroke Medium-Speed Engines

Beginning Q4 2025, Hanwha Engine will expand beyond its core low-speed engine business to produce 4-stroke medium-speed engines, diversifying its product portfolio and addressable market.

Market Entry Timeline:

- Q4 2025: Production launch

- End 2026: First deliveries

- 2027+: Full-scale earnings contribution

Capital Efficiency: The company is utilizing existing facilities, minimizing capital expenditure while maximizing incremental returns.

Competitive Moat Analysis

“Only Hyundai Heavy Industries and Hanwha Engine possess the technical capability to properly manufacture low-speed engines for large vessels. Entry barriers are exceptionally high, making new competitor emergence unlikely.”

This competitive assessment highlights several critical factors:

Technology Barriers:

- Decades of accumulated engineering expertise required

- Complex metallurgy and precision manufacturing demands

- Stringent quality and reliability standards

Market Structure Benefits:

- Supplier-advantaged market dynamics

- Stable profit structure with limited competition

- Captive volume secured through Hanwha Ocean relationship

The captive relationship with Hanwha Ocean provides predictable baseline demand, reducing revenue volatility while allowing the company to pursue external orders at favorable margins.

Investment Strategy for Hanwha Engine

Technical Analysis:

- Buy Zone: Below ₩45,000

- Price Target: ₩55,000 (22% upside potential)

- Stop Loss: ₩36,000 (risk management level)

Investment Thesis:

- Direct beneficiary of shipbuilding upcycle with superior margin profile

- DF engine mix improvement driving ASP expansion

- Portfolio diversification through medium-speed engine entry

- High barriers to entry protect market position

- Stable captive demand from Hanwha Ocean

Investment Considerations for Global Investors

Strategic Positioning Rationale

Both SPG and Hanwha Engine require mid-to-long-term investment horizons rather than short-term trading approaches. These companies represent fundamental growth stories with tangible business developments:

SPG: Strengthening position as a core component supplier in the robotics industry with clear path toward value chain expansion

Hanwha Engine: Dual momentum from shipbuilding upcycle benefits and new business segment launch

Market Timing Opportunity

While global attention concentrates on Korean semiconductors and biopharmaceuticals, robotics and shipbuilding sectors are demonstrating clear earnings improvements with less crowded investor positioning. This creates potential alpha generation opportunities for investors who recognize these trends ahead of broader market awareness.

Risk Factors to Monitor

SPG Risks:

- Humanoid robot market adoption timeline uncertainty

- Competition from established Japanese manufacturers

- Technology transition execution risk

- Customer concentration in emerging market segments

Hanwha Engine Risks:

- Shipbuilding cycle downturn vulnerability

- Raw material cost inflation

- New production line execution risk

- Dependence on global shipping demand

Portfolio Application

These stocks suit investors seeking:

- Exposure to Korean industrial innovation

- Mid-cycle recovery plays with earnings visibility

- Diversification from semiconductor concentration

- Access to robotics and maritime technology trends

Conclusion: Hidden Value in Korean Industrial Excellence

SPG and Hanwha Engine represent the type of focused, technically excellent companies that form the backbone of Korea’s advanced manufacturing economy. For global investors willing to look beyond the heavily-covered semiconductor and tech sectors, these stocks offer compelling combinations of:

- Proven technical capabilities

- Clear earnings catalysts

- Reasonable valuations relative to growth potential

- Strategic positioning in high-barrier industries

As the Korean stock market continues to attract international capital, identifying quality companies before broader discovery remains a viable strategy for alpha generation.